Legal | 4 minute read

You Finally Found Your Dream Home… Now What?

By Eliza Theiss | Feb 25, 2019

A step by step process for closing on real property in NYC NYC-based boutique law firm Pardalis & Nohavicka brings the latest legal updates from the world of real estate to PropertyShark. Pardalis & Nohavicka handles an eclectic array of matters, representing individuals and business owners in civil litigation, criminal cases and business transactions, currently litigating and representing clients throughout…

A step by step process for closing on real property in NYC

NYC-based boutique law firm Pardalis & Nohavicka brings the latest legal updates from the world of real estate to PropertyShark. Pardalis & Nohavicka handles an eclectic array of matters, representing individuals and business owners in civil litigation, criminal cases and business transactions, currently litigating and representing clients throughout the United States and around the world.

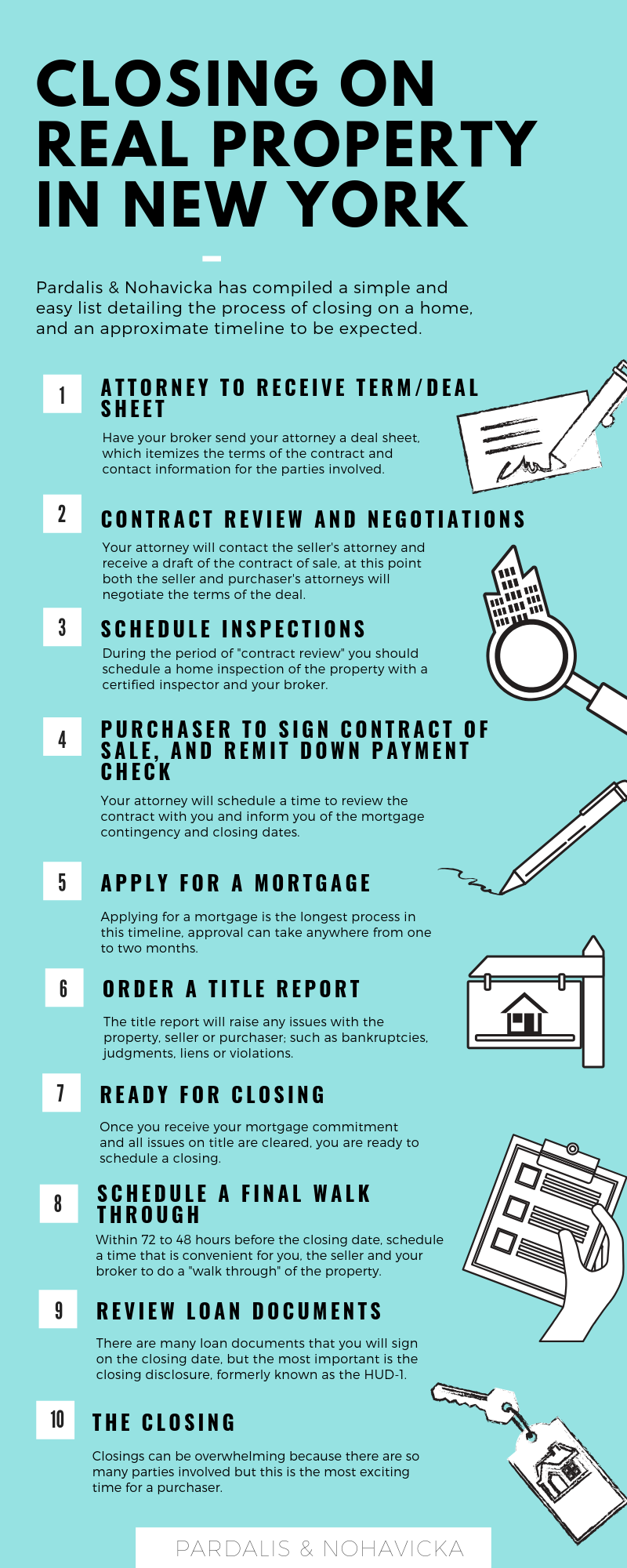

First time buyers might be nervous and confused about the home buying process, but who wouldn’t be when investing your entire life savings into a piece of real estate? Pardalis & Nohavicka has compiled a simple and easy list detailing the process of closing on a home as well as an approximate timeline. The entire process from finding a home until closing date differs greatly between deals, but it generally takes between 4 and 12 weeks, depending on whether the purchaser is obtaining a mortgage. These 10 steps give a quick overview of the whole process:

1) Attorney to Receive Term/Deal Sheet: Have your broker send your attorney a deal sheet that itemizes the terms of the contract for the parties involved. This helps the attorney to get a basic understanding of the deal and to confirm the terms with both the client and the seller’s attorney.

2) Contract Review and Negotiations: Your attorney will contact the seller’s attorney and receive a draft of the contract of sale. Then, both the seller’s and purchaser’s attorneys will negotiate the terms of the deal. Generally, contracts are fairly standard, although most attorneys add riders to their contracts depicting specific additional terms that are not already included. The most important factors to be aware of are the purchase price, proposed closing date, mortgage contingency date, and personal property included in the sale. This negotiation process could take anywhere from two days to two weeks to finalize.

3) Schedule Inspections: During the period of “contract review” you should schedule a home inspection of the property with a certified inspector and your broker. The inspector will compile a list of physical issues with the property so that you can get a better sense of what repairs might need to be done, and the condition of the property. In New York, it is the purchaser’s responsibility to be aware of the condition of the property, because the seller does not give any representations and sells “as is.”

4) Purchaser to Sign Contract of Sale, and Remit Down Payment Check: Your attorney will schedule a time to review the contract with you and inform you of the mortgage contingency and closing dates. At this time, you will sign the contract and remit a down payment check, which is usually about 10-20% of the purchase price, and is only refundable in very specific instances.

Closing on real property in New York

5) Apply for a Mortgage: Applying for a mortgage is the longest process in this timeline; approval usually takes between one to two months. It is crucial to begin the application process as soon as possible because you do not want to miss the mortgage contingency date, which is specified in the contract as the deadline for the purchaser to receive a mortgage commitment from the lender. Generally, this date is set as thirty or forty five days from the execution date of the contract. This date is crucial, because if a purchaser fails to receive a mortgage commitment on the specified date, you could potentially lose your down payment.

The lender requires a series of documents to be reviewed for approval of the loan, including tax documents, the loan application and an appraisal. An appraisal is when a certified assessor visits the property to determine its value. Not only does the appraised value determine whether a purchaser will receive the full amount of the loan they requested, it will also determine whether the sale will actually close. Most standard contracts include language that releases a purchaser from being obligated to close if the appraised value is lower than the purchase price on the contract.

6) Order a Title report: The title report will raise any issues with the property, seller or purchaser; such as bankruptcies, judgments, liens or violations. Both the seller and purchaser’s attorneys will work together to clear all issues prior to closing, for “Marketable Title.”

7) Ready For Closing: Once you receive your mortgage commitment and all issues on title are cleared, you are ready to schedule a closing.

8) Schedule a Final Walk Through: Within 72 to 48 hours before the closing date, schedule a time that is convenient for you, the seller and your broker to do a walk-through of the property. This is your chance to make sure all the repairs requested from the seller have been rectified, the seller has not left any personal belongings behind, and no material damage has been done to the property. If there are any issues with your walk-through, notify your attorney before the closing date.

9) Review Loan Documents: There are many loan documents that you will sign on the closing date, but the most important is the closing disclosure, formerly known as the HUD-1. The closing disclosure lists all of the fees incurred for the closing and how the proceeds of the loan are disbursed.

10) The Closing: Closings can be overwhelming because there are so many parties involved, but this is the most exciting time for a purchaser. At the closing, you will sig

n loan documents, including your note, mortgage and closing disclosure. You will also sign transfer documents, and receive your title insurance and loan insurance policies. Finally, you will receive all keys and codes to the property – it’s finally yours!

Just a few extra points: these steps can differ by state and by the type of property. For example, the purchase of a condo or co-op will differ from the purchase of a 1-4 family home.

About

Expert insight and analysis was provided by Real Estate and Corporate Transactions Attorney Nataly Goldstein and Partner Taso Pardalis of Pardalis & Nohavicka, LLP, . Nataly is a graduate of Cardozo School of Law, where she served as President of the Real Estate Law Association. She is experienced in both residential and commercial real estate transactions, as well as representing large banks, such as Wells Fargo and Citibank.

Expert insight and analysis was provided by Real Estate and Corporate Transactions Attorney Nataly Goldstein and Partner Taso Pardalis of Pardalis & Nohavicka, LLP, . Nataly is a graduate of Cardozo School of Law, where she served as President of the Real Estate Law Association. She is experienced in both residential and commercial real estate transactions, as well as representing large banks, such as Wells Fargo and Citibank.

Latest Posts

Want to stay on top of the real estate market?

Access comprehensive property data and ownership information with intuitive research tools.

Eliza Theiss is a senior writer reporting real estate trends in the US. Her work has been cited by CBS News, Curbed, The Los Angeles Times, and Forbes among others. With an academic background in journalism, Eliza has been covering real estate since 2012. Before joining PropertyShark, Eliza was an associate editor at Multi-Housing News and Commercial Property Executive. She has also contributed extensively to CommercialEdge. Reach her at [email protected]

Recent Reports

Locked-In Owners, Mobile Renters: Homeowners Stay Put as Renters Move 3.7x More Across Largest U.S. Cities

Renters became the primary drivers of long-distance mobility across the largest U.S. cities, moving 3.7 times more than owners in 2024, as high mortgage rates and housing costs kept many homeowners in place.

$4.6M Hudson Yards Maintains Top Spot, Luxury Sales in Malba Set $2.5M Price Record for Queens

Despite prices declining, Hudson Yards remained the most expensive NYC neighborhood, but TriBeCa’s growth closed the gap to under $400,000, while Malba set a new historic price record for Queens at $2.5 million, securing the highest ranking ever for the borough at #5.

2026 Q1 Foreclosure Report: Brooklyn Filings Fall Sharply, Bronx & Staten Island Hit New Peaks

Behind a deceptively mild citywide downtick, borough foreclosure markets pulled into significantly diverging paths as Brooklyn cases were nearly halved and the Bronx hit a new, record high. Meanwhile, Queens remained unchanged, Staten Island surged back up and Manhattan cooled slowly.