RELEASED ON July 30, 2018

How Much Money Are You Left with Each Month After Paying All Expenses?

Robert Demeter | 10 minute read

Key Takeaways: As an owner, you can save more than $4.5k/month in Manhattan and $3.5k in San Jose; Having the second-highest median income in the country, homeowners can save $2.6k in SF; With low living and housing costs, residents in Raleigh and Austin can save over $2k per month; Miami leaves a hole of more than $1.2k in the pockets of homeowners; As a renter, you can save the most money in Virginia Beach: $883; Renters have it the hardest in Brooklyn and Boston, where each month a $2k+ debt accumulates; Median household income varies from city to city, and in places where the average worker gets paid more, rents and home prices are generally higher. U.S. homeowners can often save money once housing costs and living necessities are covered. By contrast, renters can barely get by in some cities if they don’t seriously cut on their expenses—or find a roommate. One reason behind this discrepancy is that homeowners tend to be older than renters, and hence earn more money since work experience translates into higher salaries. Owner-occupied households are also formed by a higher percentage of married people, and it is easier for two people to save up than…

Key Takeaways:

- As an owner, you can save more than $4.5k/month in Manhattan and $3.5k in San Jose;

- Having the second-highest median income in the country, homeowners can save $2.6k in SF;

- With low living and housing costs, residents in Raleigh and Austin can save over $2k per month;

- Miami leaves a hole of more than $1.2k in the pockets of homeowners;

- As a renter, you can save the most money in Virginia Beach: $883;

- Renters have it the hardest in Brooklyn and Boston, where each month a $2k+ debt accumulates;

Median household income varies from city to city, and in places where the average worker gets paid more, rents and home prices are generally higher. U.S. homeowners can often save money once housing costs and living necessities are covered. By contrast, renters can barely get by in some cities if they don’t seriously cut on their expenses—or find a roommate. One reason behind this discrepancy is that homeowners tend to be older than renters, and hence earn more money since work experience translates into higher salaries. Owner-occupied households are also formed by a higher percentage of married people, and it is easier for two people to save up than for a single renter.

PropertyShark and RENTCafé joined forces to carry out a study on discretionary income and analyzed the top 50 largest cities (52 actually, as Manhattan, Brooklyn and Queens have been considered individually) in which an owner or a renter can save the most money after paying living costs. We determined the discretionary income in each city by subtracting living and housing costs from the median household income. The median household income of a homeowner and a renter as well as housing costs were extracted from Census data, while living costs, such as food, healthcare, entertainment, and transportation were taken from U.S. Department of Labor. Rent data was provided by RENTCafé.

In 44 out of the 50 cities highlighted in our study, homeowners can save money each month. Some can even apply the 50/30/20 budget scheme, where 50% represents money spent on needs, such as housing costs, bills, taxes and living essentials, 30% spent on wants and 20% allocated on savings and investments. In fact, only in cities such as Miami, Detroit or Philly do you have to seriously cut expenses to make it through the month without accumulating debt. But as a renter, you can easily end up having too much month left at the end of your money in more than half of the cities in our study.

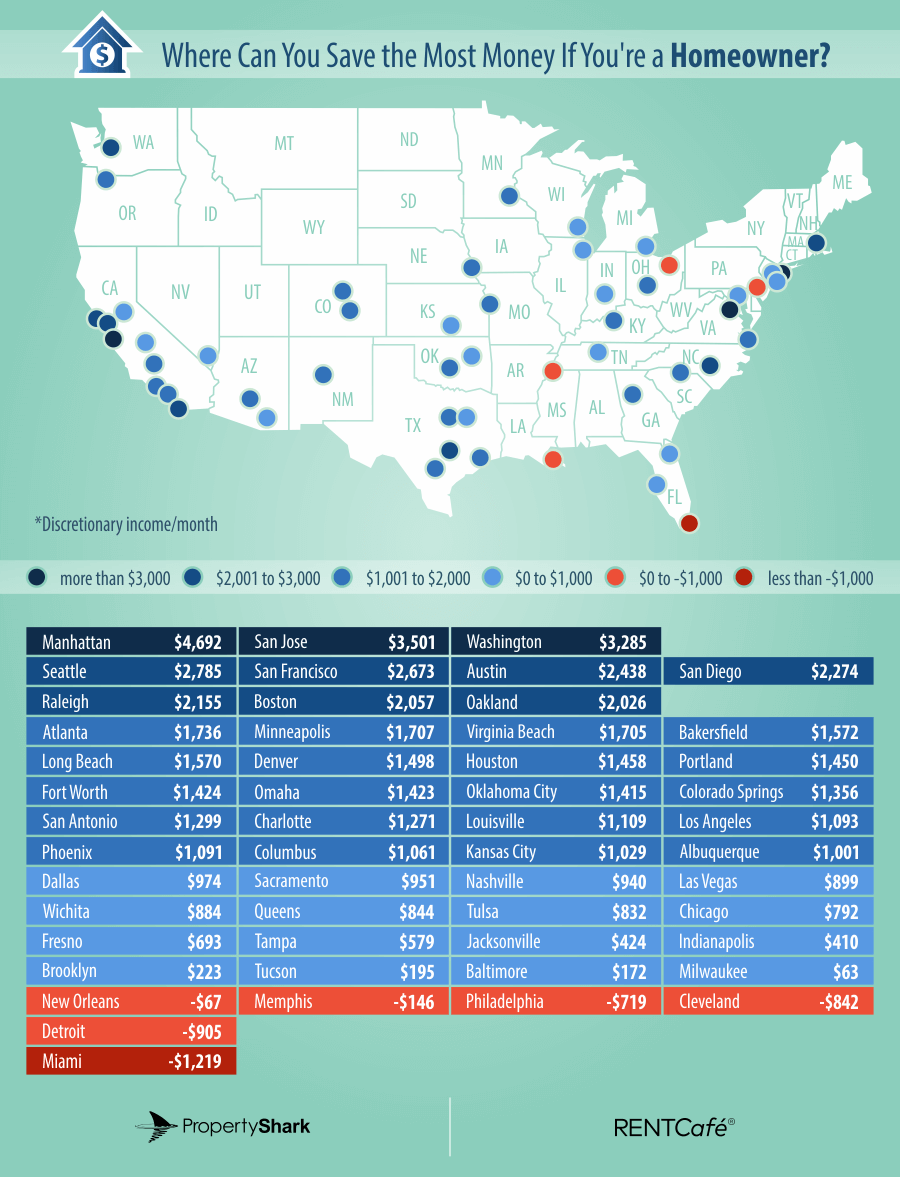

After Paying All Expenses, You Can Save More Than $4.5K/Month in Manhattan as an Owner

If you jumped through hoops and finally managed to save on a down payment in Manhattan, the hard part is over. The NYC borough ranks as #1 when it comes to saving money as an owner and boasts the largest median household income out of the 50 cities: $11,837/ month.

Manhattan’s financial sector no doubt boosts the median household income of residents, but there’s also a hefty price to pay to live in America’s hottest location. Owner living costs are the highest in the nation at $5,259/month, while housing costs reach a median of $1,886. After paying for all necessities, leisure goods and services each month, owners earning the median salary in the NYC borough are left with $4,692—the most money in the country.

Over on the West Coast, San Jose lands the second spot on our list. High-paying jobs in the information, education and healthcare sectors have a positive impact on the Silicon Valley city’s median salaries, although housing costs are more expensive compared to Manhattan. Out of the total $9,834 median household income, the average San Jose owner pays $2,282 for housing and $4,051 for living costs, with $3,501 remaining each month in their pocket— about $900 more than you can save just a couple of miles north, in San Francisco ($2,673).

At $5,079, The Golden Gate City has the #1 most expensive housing costs and at the same time has the 5th highest living costs. If it weren’t for these extremes in costs of living, San Francisco could have ended up as a runner-up to Manhattan, as its median income ($10,151) is the second-highest in the country after the NYC borough.

The two other cities which round out our top 5 include Washington D.C. on third place and Seattle on fourth. With a median household income of $9,850, you can save $3,285 after paying the $1,929 housing costs and spending $4,636 on needs in the capital city. In Seattle, a homeowner can put $2,785 under the mattress each month, after paying housing and living expenses.

All of the cities in the top 5 have median household incomes of over $9,000/per month, suggesting that people can save the most where income is the highest. However, there are some exceptions.

Austin and Raleigh Land Spots in the Top 10 for Having Low Housing and Living Costs

With lower incomes, these two state capitals cities ended up on the 6th and 8th positions, respectively, thanks to very affordable living and housing costs compared to the median household income.

With a $7,679 median salary, an Austin resident can save up to $2,438 each month after paying only $1,474 for housing and spending $3,767 on living expenses. Austin is still the most expensive city in Texas, but compared to other large cities in the nation, it stands out as highly affordable, at least for median income earners.

In Raleigh, you can set aside $2,115 after paying monthly living and housing costs. At $1,273 per month, housing costs are extremely low compared to other cities on our list, while living costs equate to $3,670.

The additional 3 cities in our top 10 where owners can save the most money include San Diego ($2,274), Boston ($2,057) and Oakland ($2,026).

Income Is Solid, But High-Costs Are a Drag on Savings in Brooklyn, LA and Long Beach

The median household income in both Los Angeles and Long Beach is above $7,000, but expensive housing and living costs prevent homeowners from saving more. Alas, with a median income of $7,315 in Long Beach, after paying $1,780 on housing and covering the $3,965 median expenses, owners are left with $1,570. In Los Angeles, income is slightly lower, and living and housing costs are higher, with homeowners being able to save only $1,093.

In Brooklyn, things aren’t very bright when it comes to building up that savings account. Even though living in this borough costs almost the same as living in Manhattan, the median income is considerably lower. At $6,978, median income in Brooklyn is just 59% of what an average Manhattan resident makes in one month. After paying expenses and housing costs, you’ll end up with only $223 in your pocket. While this may seem paltry, typical homeowners in cities at the bottom of the list are sliding straight into debt.

Miami Leaves a Hole of More Than $1.2K in the Pockets of Homeowners Each Month

In Miami, Detroit, Cleveland, and Philly, homeowners struggle to save. Memphis and New Orleans also fall in this category, although spending below the median costs helps you achieve a sustainable living.

Miami sits at the bottom of the list, with very low median household income ($4,241) compared to similar cities and living costs exceeding $4,274. Adding housing costs to the mix ($1,186), monthly expenditures leave the average Miami homeowner with a debt of $1,219 each month. With living costs already higher than the median income, you’d have to drastically cut your expenses to afford living in the city.

The situation in Detroit isn’t bright either, where the median household income of $3,204 isn’t enough for paying monthly essentials and housing costs, let alone saving, leaving the owner with a hole of $905 each month.

In Cleveland and Philadelphia, homeowners struggle as well. The median household income in Cleveland is $3,536, just about the equivalent to the monthly living costs, which equates to $3,647, leaving the average resident in a $842 debt if they don’t cut on expenses. In Philadelphia, the average owner accrues $719 more in debt each month.

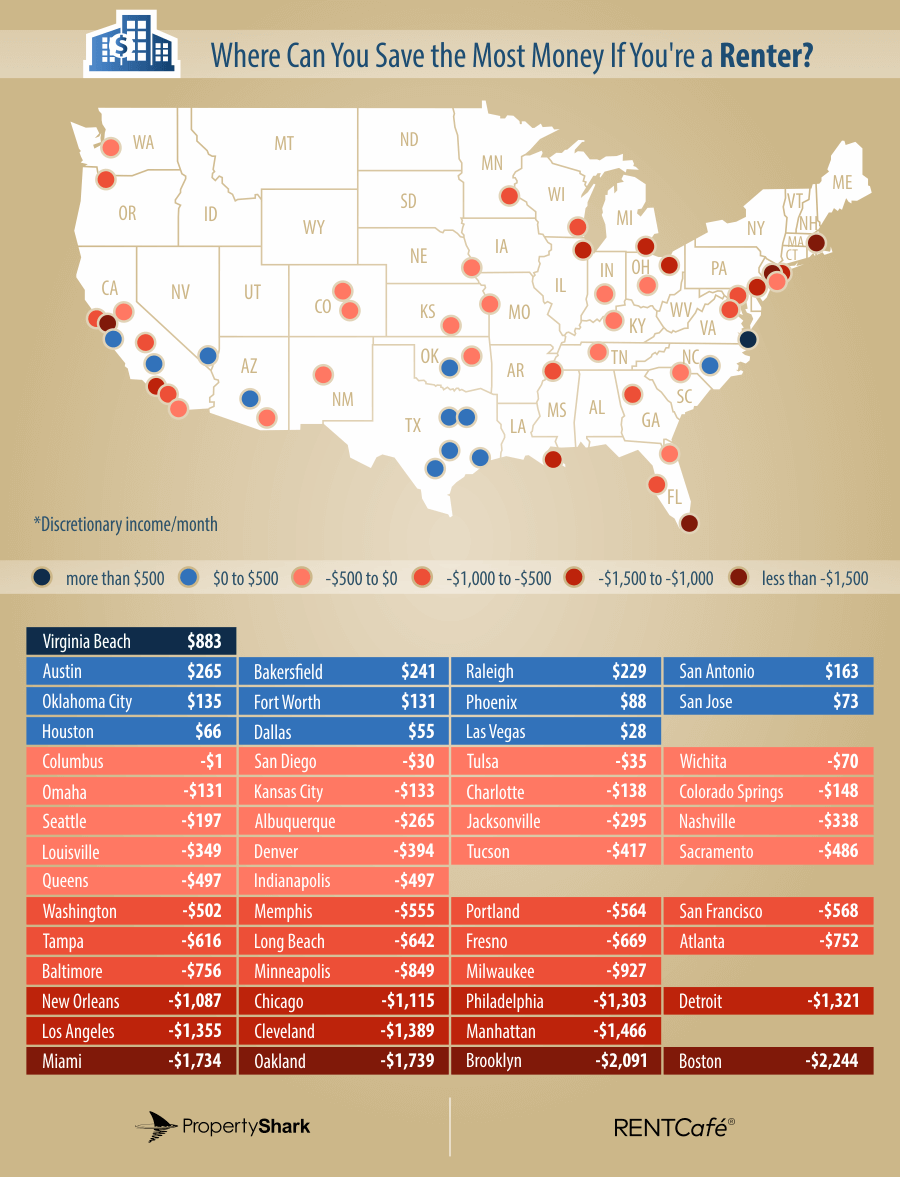

Renters Have It Far Worse Than Owners

Out of the 50 cities, there are only 4 where a renter earning the median income can actually save a decent amount of money after covering rent and living, and not because of high income but as a result of a healthy balance between the median income, rent and living costs. As opposed to homeowners, a large median income doesn’t always guarantee an easier life for renters, due to extremely high costs.

In most cities, you can get by just fine as an owner and save an impressive amount of money. But as a renter, if you don’t cut your expenses or have a roommate, monthly costs in 31 cities could leave you spending all of your income, forcing you into debt. In the bottom 11 cities it gets even worse, if you don’t spend drastically below the median costs. Renting in Philadelphia apartments leaves you with a $1,300 deficit at the end of the month, and renters in Miami are $1,700 in debt after paying for all their expenses.

Let’s take a closer look at the stats provided by RENTCafé on the median rent of the 50+ largest U.S. cities to see how renters fare in comparison to owners.

Virginia Beach Is the #1 Most Affordable Location for Renters

The coastal city in southeastern Virginia is among the locations where the monthly median household income for a renter is quite high ($4,064). After paying both rent and monthly expenses, you’ll end up with a surplus of $883, the most money you can save as a renter in any of the 50 cities.

Renters in Austin and Raleigh can set aside a small amount at the end of each month, although not as much as owners can in these two cities. In Austin, you’d be left with $265 out of $3,578 by the end of the month, while in Raleigh you add $229 to your piggy bank.

Renters in the other 4 Texas cities on our list are also able to save a bit of cash each month. In San Antonio, a renter can set aside $163, in Fort Worth $131, in Houston $66 and $55 in Dallas. By spending less than the median on living costs and by getting a roommate, you can seriously up your savings game here.

Saving in San Diego, Charlotte and Seattle is Possible by Reducing Expenses

Even though income is high in these cities, expensive rents and living costs prevent renters from saving money without giving up on certain expenditures. Living in a house for rent in San Diego would leave you with -$30 at the end of the month after paying everything from rent to taxes and living costs, but $30 is a pretty easy hole to fill with a little bit of saving.

In Charlotte, where the median income sits at $3,181, a typical renter would have to borrow $138 each month, while in Seattle, you’d have to keep an eye on your money to not end up $197 short. Tulsa, Kansas City and Colorado Springs also fall into this category, where a renter ends up with deficits between $100 and $200 each month.

In Brooklyn & Boston You Can Save as a Homeowner, but Can’t Afford to Live as a Renter

Boston sits at the bottom of the list, and a renter in this city is likely to take on a lot of debt. With an income of $3,397, and after paying the $3,175 median rent, you’d only end up with a couple of bucks to put towards your $2,466 of living costs, leaving the average renter with a mind-boggling debt of $2,244/month. No matter how much you’d try to save, it’s impossible to live as a single renter in the city by earning just the median household income, and even with someone to share the rent, saving would be an uphill battle.

The same goes for Brooklyn, where no amount of saving can get you out of the -$2,091 deficit, unless you share your rent with 2 or 3 people.

In Manhattan, where rents are the highest in the country at $3,700, not even a $5,000+ income can save you from going into debt if you don’t drastically cut your expenses and get a roommate. Nonetheless, a renter in Manhattan is still better off than one in Brooklyn, thanks to higher incomes.

High apartment rents in Oakland and Los Angeles also put these 2 Californian cities in the top 10 most unaffordable for renters. San Francisco renters, on the other hand, are in slightly better financial shape because incomes are significantly higher here.

While the median household income in these cities is higher, extreme rent costs make them unaffordable. In New Orleans, Detroit, and Cleveland it’s the exact opposite: rents are low, around $800 – $900 per month, but the median household income is very low, between $1,500 and $2,000, making it difficult for renters to afford both rent and living costs.

Rent or Own?

The discrepancy between what owners and renters are saving in some cities is huge. It’s understandable that renters earn less and are usually single, while a higher percentage of owners are married and have a heftier income, but just by looking at the numbers and sometimes seeing thousand-dollar differences is staggering.

“One of the biggest culprits behind the heavy housing cost burden is the fact that incomes have not increased at the same pace as housing prices, creating an affordability problem nationwide. Apartment rents have accelerated during and after the recession, as demand for rentals has surged. Renters who live in the most expensive markets in the U.S., New York, Boston, and the Bay Area, are particularly affected by these disproportionate changes in income versus rents,” Nadia Balint, Senior Marketing Writer, RENTCafé.

For single renters, saving money while earning the median household income seems impossible in most cities, and in those cases where you can save, the amount is quite low. While the situation seems bleak at first glance, there are cities where you can have a sustainable lifestyle without worrying about debt by spending less than the median on living costs. Cutting down on entertainment and eating out less frequently, for example, can sometimes make the difference between running out of money and making ends meet.

Owners have it generally better than renters and can save in almost any city without cutting monthly expenditures—but there are a few exceptions. The tough part for a homeowner comes before he even owns a home: the moment you start saving for a down payment, which if you’re a renter in some of the least renter-friendly cities, you’ll most definitely have a hard time saving.

Methodology

We determined the discretionary income by subtracting living and housing costs from the median household income. The median household income was extracted from Census, separately for homeowners and renters.

Living costs were calculated by multiplying the monthly national living costs—which are calculated by the U.S. Department of Labor—with the NUMBEO Cost of Living Index. Living costs include everything from food to childcare, sports and leisure, transportation, healthcare, entertainment, personal care and services, reading, education, tobacco products and smoking supplies, cash contributions and personal insurance and pensions and other miscellaneous costs.

Rent data, which consists of median rent for multifamily properties of 50 or more units, was provided by RENTCafé.

The list contains top 50 U.S. cities by population. Please note that we split NYC in Manhattan, Brooklyn and Queens.

Want to stay on top of the real estate market?

Access comprehensive property data and ownership information with intuitive research tools.

POSTED IN: Market Studies, National

Robert is a copywriter at CommercialCafe and brings 3+ years of experience in commercial real estate. He previously worked as a copywriter at PropertyShark, as a senior associate editor at Commercial Property Executive and Multi-Housing News, and also wrote monthly market reports at Yardi Matrix.

Recent Reports

World Cup or Your Mortgage/Rent? Ticket Prices Rival Host City Housing Costs

World Cup ticket prices rival monthly housing expenses in the 11 U.S. host cities, with even the cheapest seats covering weeks or even months of rent or mortgage payments.

Locked-In Owners, Mobile Renters: Homeowners Stay Put as Renters Move 3.7x More Across Largest U.S. Cities

Renters became the primary drivers of long-distance mobility across the largest U.S. cities, moving 3.7 times more than owners in 2024, as high mortgage rates and housing costs kept many homeowners in place.

$4.6M Hudson Yards Maintains Top Spot, Luxury Sales in Malba Set $2.5M Price Record for Queens

Despite prices declining, Hudson Yards remained the most expensive NYC neighborhood, but TriBeCa’s growth closed the gap to under $400,000, while Malba set a new historic price record for Queens at $2.5 million, securing the highest ranking ever for the borough at #5.